Chris Clark

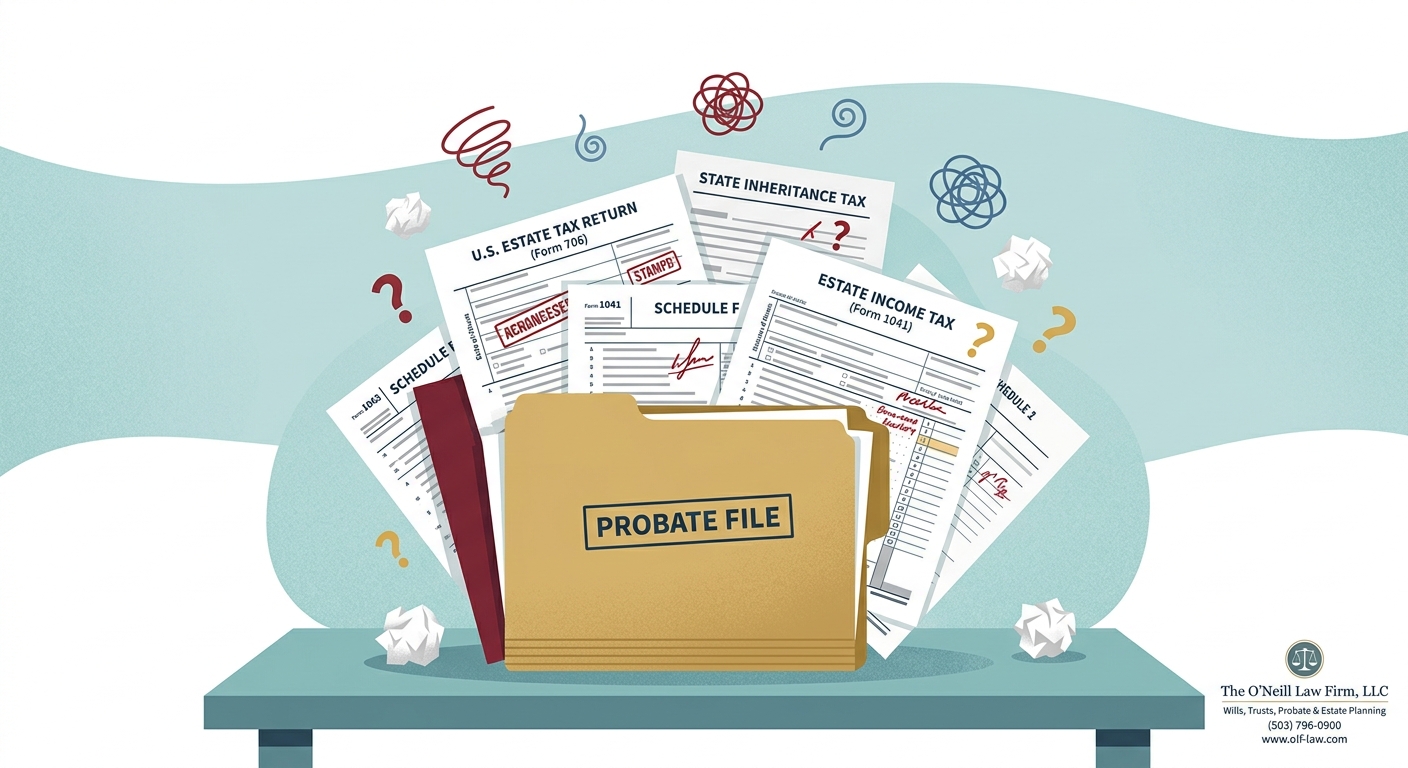

Protecting the Personal Representative from Unfiled or Unpaid Taxes in an Oregon Probate

Benjamin Franklin once said, "In this world nothing can be said to be certain, except death and taxes." But sometimes, taxes aren't so certain -- especially when a personal representative of a decedent's estate discovers that the decedent hadn't filed all required returns or paid all required taxes. Below are some strategies for the personal representative to consider with their advisor to prevent the decedent's tax problems from becoming their own.

Ask the taxman

The personal representative can request the decedent's tax records from the IRS by using Form 4506-T with proper proof of authorization. Those records requested by this form can show if a return was filed for a given tax year and if there any unpaid taxes that have been assessed. The IRS can also provide a list of all W-2 and 1099 filed with the IRS for a given year. These reports may not show all possible sources of income, but it is often a good start. In Oregon, a qualified representative can obtain similar information about a decedent's tax filing status and unpaid assessed taxes by contacting the Oregon Department of Revenue and providing appropriate proof of authority (e.g., a death certificate and Letters of Administration/Testamentary).

File unfiled tax returns that the decedent should have filed, but didn't

Tax authorities typically have 3 years after a tax return is due to assess additional taxes (there are exceptions with longer limitations periods). However, if no tax return was filed for a return that was due, the statute of limitations never starts. The tax authorities will look to the decedent's personal representative to file that return, and can hold the personal representative liable if for unpaid taxes if the return is not filed.

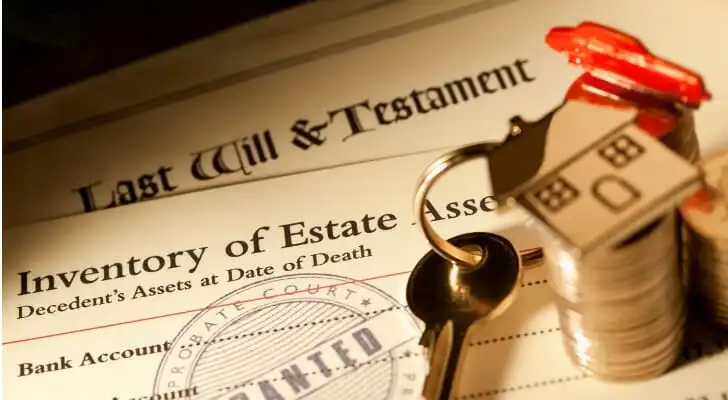

Pay expenses and debts in the right order

If there are not enough funds in the estate and/or trust to pay the taxes owed, the personal representative must take care to pay expenses and debts of the decedent in the priority prescribed by law. Taxes have a higher priority over many other creditors, but are lower in priority than other expenses. If the personal representative runs out of funds in an estate paying lower-priority creditors but still has taxes owed, the personal representative will be personally liable to the extent they paid lower-priority creditors. Consulting with an attorney to understand the priority of probate expenses and waiting to pay creditors until after understanding the decedent's tax liability can help avoid this difficult situation.

Get released from liability

The personal representative can request the tax authorities to release them from personal liability for many types of taxes. IRS Form 5495 is used for federal income taxes, and Oregon Form OR-DECD-TAX is used for this purpose for Oregon income taxes (by checking the correct box). While there are exceptions, these forms release the fiduciary from personal liability within nine months after the filing of the form (or within nine months from the due date of the relevant tax return) if no notice of deficiency is received during that time. For federal estate tax, IRS Form 5495 is also used and has a nine-month limitations period. Oregon Form OR-706-DISC is used for the Oregon estate tax; it has an 18-month limitations period. Importantly, if the personal representative is also the beneficiary, the protection afforded by these forms is limited because of transferee liability.

Shorten the statute of limitations

The personal representative can ask to shorten the normal 3-year statute of limitations for many income tax returns to 18-months. For this purpose, IRS Form 4810 is used federal income taxes, and Oregon Form OR-DECD-TAX is used for Oregon (by checking the correct box). If no assessment for the tax year for which the election is made within the 18-month limitations period, then no further assessments can be made. In Oregon, there are some assessments that can be made even after the 18-month limitation period expires (e.g., a false or fraudulent return; a federal change to tax liability is made).

Administering a loved-one's estate can be a difficult job at a difficult time, and taxes can add to that burden. Getting tax and legal advice from qualified advisors and timely filing the right tax forms can help make that job easier.

Protecting the Personal Representative from Unfiled or Unpaid Taxes in an Oregon Probate

How New Tax Incentives Can Boost Your Charitable Giving

Tricks and Traps in Managing an Insolvent Probate Estate in Portland

Don’t Forget Your Beneficiary Designations

Taxes in Probate: The Essentials

How Life Changes Reshape Your Estate Plan

Choosing a Guardian: Myths and Realities

Essential Legal Documents for Turning 18

Stay Alert: Common Scams Targeting Seniors

Probate Responsibilities: Handling Decedent Taxes in Portland

Updating Your Estate Plan for New Family Members

Spring Cleaning Your Estate Plan: A Fresh Start